The Paycheck-to-Paycheck Cycle Is Exhausting.

Living paycheck to paycheck is not just a money problem. It is a stress problem.

It means every payday feels like relief, but only for a moment. The money arrives, bills attack it immediately, food and transport take another portion, debt payments remove more, and within days you are already counting down to the next paycheck.

That cycle is painful because it makes you feel like you are working only to survive.

You may ask yourself:

- Why does my money disappear so fast?

- Why can’t I save even a small amount?

- Why do emergencies always destroy my budget?

- Why does every month feel the same?

- Why do I earn money but never seem to move forward?

The answer is not always laziness. Sometimes the problem is low income. Sometimes it is debt. Sometimes it is inflation. Sometimes it is family responsibilities. But very often, the problem is also the absence of a working system.

If you want to learn how to stop living paycheck to paycheck, you need more than motivation. You need a practical budget system that controls your money before your money disappears.

This article gives you that system.

It will show you how to organize your paycheck, prioritize bills, control spending, build a small buffer, reduce financial pressure, and slowly create breathing room.

This is not a fantasy plan. It is realistic. It works best when repeated consistently.

“If you want a proven step-by-step system to break the paycheck to paycheck cycle for good, “Broke Millennial: Stop Scraping By and Get Your Financial Life Together” by Erin Lowry is the most recommended starting point for beginners.”

What Does Living Paycheck to Paycheck Mean?

Living paycheck to paycheck means most or all of your income is spent before the next paycheck arrives.

You may have little or no savings. You may rely on credit, loans, overdrafts, or borrowing from friends and family when unexpected expenses happen. Even if you earn a decent income, you may still feel financially trapped because your expenses rise to match your earnings.

The paycheck-to-paycheck cycle usually looks like this:

- Payday arrives.

- Bills and debt payments take a large portion.

- Food, transport, and daily expenses take more.

- Small unplanned purchases reduce what is left.

- An unexpected expense appears.

- You borrow, delay a payment, or use credit.

- The next paycheck is already partly committed.

- The cycle repeats.

The dangerous part is that this cycle can become normal. You start accepting financial pressure as a permanent condition.

But it does not have to be permanent.

To break the cycle, you need to change what happens immediately after money comes in.

That is where a practical budget system becomes powerful.

Why Most People Stay Stuck Between Paychecks

Before fixing the problem, you need to understand what keeps the cycle alive.

Most people stay paycheck to paycheck because of a mix of these issues:

- Income is too low for current expenses

- Bills are not planned before spending begins

- Debt payments consume future income

- Small expenses are not tracked

- Savings happen last instead of first

- Emergencies are handled with borrowing

- Spending is emotional or impulsive

- Lifestyle upgrades happen too quickly

- Irregular expenses are ignored

- There is no weekly money review

A common mistake is blaming one thing.

People say:

“My rent is too high.”

“My income is too low.”

“Food is expensive.”

“I just need a better job.”

“I’m bad with money.”

Some of those may be true, but they are incomplete.

If you want to know how to stop living paycheck to paycheck, you need to treat your money like a system. Income, bills, savings, debt, spending, habits, and planning all work together. If one part is weak, the whole system suffers.

The goal is not to create a perfect financial life in one month. The goal is to create enough order that you are no longer constantly reacting.

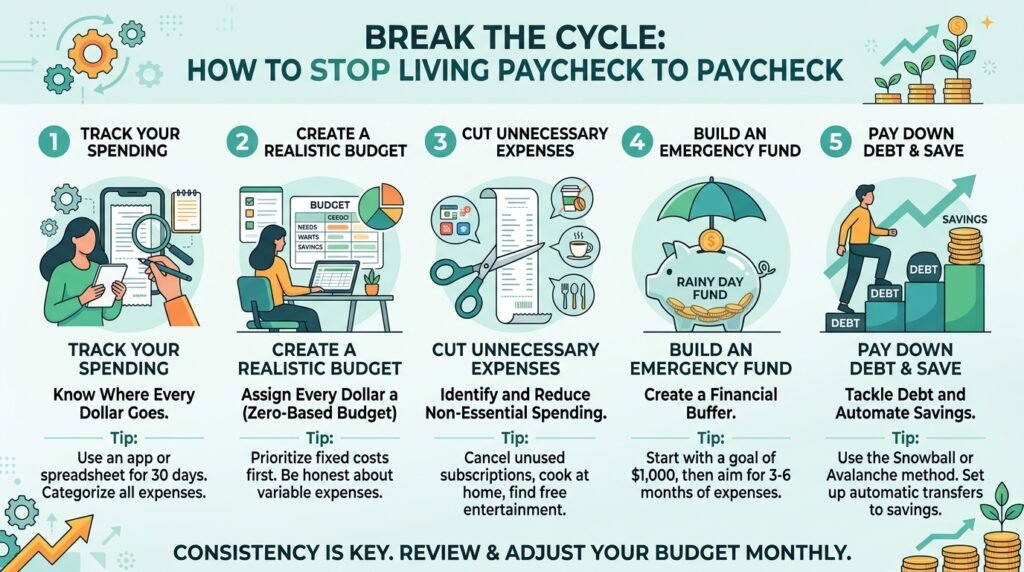

The Practical Budget System That Breaks the Cycle

This system has five parts:

- Paycheck mapping — knowing exactly where your income must go

- Priority budgeting — funding needs before wants

- Weekly spending control — stopping money from disappearing too early

- Small buffer building — creating protection from emergencies

- Paycheck gap expansion — slowly increasing the number of days your money lasts

This system works because it does not depend on perfect discipline. It gives your money structure before temptation, pressure, or confusion can take over.

A weak budget says, “I hope I spend less this month.”

A strong budget says, “This money already has a job.”

That difference is everything.

Step 1: Face the Real Numbers

You cannot stop living paycheck to paycheck if you do not know your real numbers.

This step is uncomfortable, but necessary.

Write down your monthly income first.

Include:

- Salary

- Wages

- Freelance income

- Business income

- Side hustle income

- Commissions

- Tips

- Support payments

- Any other regular income

If your income changes, use your lowest realistic monthly income. Do not build your budget around your best month. That creates false confidence.

Next, write down all expenses.

Start with fixed expenses:

- Rent or housing

- Utilities

- Phone

- Internet

- Insurance

- Loan payments

- Subscription payments

- School fees

- Childcare

- Minimum debt payments

Then write variable expenses:

- Food

- Transport

- Personal care

- Household items

- Data or airtime

- Medical costs

- Family support

- Entertainment

- Eating out

- Miscellaneous spending

Finally, list debt:

- Credit cards

- Personal loans

- Payday loans

- Informal loans

- Overdrafts

- Buy-now-pay-later payments

- Money owed to friends or family

This gives you your financial truth.

Do not soften the numbers. Do not guess too low. Do not hide expenses because they embarrass you.

A budget built on false numbers will fail.

Step 2: Create a Paycheck Map

A paycheck map shows where your money goes before you spend it.

This is different from a normal monthly budget because it focuses on timing.

Many people technically earn enough to cover their expenses, but they still struggle because bills arrive before money is available. That timing problem creates stress.

To create a paycheck map, divide your expenses by due date.

For each bill, write:

- Name of bill

- Amount

- Due date

- Which paycheck will pay it

Example:

| Bill | Amount | Due Date | Paid From |

| Rent | $500 | 1st | Paycheck 1 |

| Utilities | $80 | 5th | Paycheck 1 |

| Phone | $40 | 10th | Paycheck 1 |

| Loan | $100 | 15th | Paycheck 2 |

| Internet | $50 | 20th | Paycheck 2 |

| Savings | $50 | Payday | Paycheck 1 and 2 |

This helps you stop treating your paycheck like free money.

When money arrives, part of it already belongs to future bills. Your job is to protect that money before it is accidentally spent.

This is one of the most important parts of how to stop living paycheck to paycheck because many people are not broke from one big mistake. They are broke because they spend bill money before the bill is due.

Step 3: Use the Four-Bucket Budget

A complicated budget will not help if you are already overwhelmed.

Use four buckets:

- Bills

- Needs

- Savings

- Flexible spending

That is enough to start.

Bucket 1: Bills

This includes fixed obligations:

- Rent

- Utilities

- Debt payments

- Insurance

- Phone

- Internet

- School fees

Bills should be separated immediately when income arrives.

Bucket 2: Needs

These are required living expenses:

- Food

- Transport

- Medicine

- Basic household items

- Work or school necessities

Bucket 3: Savings

This includes:

- Emergency fund

- Short-term savings

- Sinking funds for future expenses

Even if you can only save a small amount, keep this bucket active.

Bucket 4: Flexible Spending

This includes:

- Eating out

- Entertainment

- Shopping

- Personal treats

- Social spending

This bucket must have a limit. If it does not, it will invade every other bucket.

This four-bucket system is simple enough to use consistently.

If you are new to budgeting, read budgeting for beginners before building a more aggressive paycheck system.

Step 4: Pay Yourself First, Even If the Amount Is Small

Many people think they cannot save because they live paycheck to paycheck.

But if you wait until the end of the pay period to save, you will almost always fail.

Savings must happen early.

This does not mean saving a large amount immediately. It means saving something first, before flexible spending begins.

Start with one of these:

- $5 per paycheck

- $10 per paycheck

- 1% of income

- 3% of income

- 5% of income

The amount can grow later. The first goal is to build the habit.

If you receive $500 and save $10 immediately, you have changed the order of your financial life. You are no longer asking, “What is left?” You are saying, “This part is protected.”

That mindset matters.

If you want to stop living paycheck to paycheck, the first savings target should be small and achievable.

Start with:

- $50

- Then $100

- Then $250

- Then $500

- Then $1,000

If your first goal is building a starter buffer, read how to save $1,000 fast.

Step 5: Build a One-Paycheck Buffer

The strongest way to escape the paycheck-to-paycheck cycle is to build a buffer.

A buffer is money that sits between you and the next paycheck.

At first, your goal is not a full emergency fund. Your first goal is a small gap.

Start with a one-day buffer.

That means you have enough money to cover one day of basic expenses without depending on tomorrow’s income.

Then build:

- 3-day buffer

- 1-week buffer

- 2-week buffer

- 1-month buffer

This is how you slowly stop living right on the edge.

A one-month buffer means this month’s income pays next month’s expenses. That is the real escape point. But do not start there if you are currently at zero. Build gradually.

Example:

If your basic monthly expenses are $1,200, your daily basic cost is about $40.

A one-day buffer is $40.

A three-day buffer is $120.

A one-week buffer is about $280.

A one-month buffer is $1,200.

The first $40 matters. The first $100 matters. Do not disrespect small progress.

For a deeper emergency savings plan, read the emergency fund guide.

Step 6: Stop Spending the Whole Paycheck in the First Week

A major paycheck-to-paycheck problem is spending too much too early.

Many people feel rich on payday and broke seven days later.

The solution is weekly spending control.

Instead of looking at the whole paycheck as available money, divide flexible spending by week.

Example:

After bills, savings, food, and transport are handled, you have $200 for flexible spending for the month.

Do not spend the $200 freely.

Divide it:

- Week 1: $50

- Week 2: $50

- Week 3: $50

- Week 4: $50

This prevents early overspending.

If you spend $120 in week one, you have created pressure for the rest of the month. Then you may borrow, use credit, or pull from savings. That keeps the cycle alive.

A weekly limit creates discipline without needing constant mental effort.

If your flexible spending money runs out, spending stops until the next week.

Harsh? Maybe.

Effective? Yes.

Step 7: Create a Bill Calendar

Bills become stressful when they surprise you.

A bill calendar solves this.

Use a notebook, phone calendar, spreadsheet, or wall calendar.

Write down:

- Payday dates

- Rent due date

- Utility due dates

- Debt payment dates

- Subscription renewal dates

- Insurance due dates

- School fee dates

- Any irregular expense dates

Then set reminders several days before each major bill.

This helps you prepare before the due date.

Many people lose money through late fees, penalties, reconnection fees, and emergency borrowing because they failed to plan around dates. That is unnecessary damage.

A bill calendar also shows which part of the month is most expensive.

If too many bills fall near one paycheck, contact providers and ask whether due dates can be changed. Not every company will agree, but some may.

Changing bill dates can reduce pressure.

Step 8: Cut Cash Leaks Before Cutting Joy

Most budget advice is too aggressive. It tells people to cut everything enjoyable.

That often fails.

A better strategy is to cut cash leaks first.

Cash leaks are expenses that take money but do not give enough value back.

Examples:

- Subscriptions you barely use

- Food delivery when groceries are available

- Daily snacks bought out of habit

- Bank fees from poor planning

- Transport costs caused by lateness

- Random online purchases

- Duplicate services

- Data waste from poor usage control

- Convenience purchases

Cutting joy makes you resent the budget.

Cutting leaks makes you stronger.

Do a cash leak audit:

- Review the last 30 days of spending.

- Highlight every expense you do not remember clearly.

- Highlight every expense you regret.

- Highlight every repeated small expense.

- Choose three to reduce this month.

Do not try to fix everything at once.

Pick the leaks with the highest frequency.

If one daily expense costs $3, that is about $90 per month. Cutting or reducing it can create real breathing room.

For more saving tactics, read how to save money fast on a low income.

Step 9: Use Sinking Funds for Predictable Expenses

Some expenses are not monthly, but they are still predictable.

Examples:

- Car repairs

- School fees

- Clothing

- Medical checkups

- Annual subscriptions

- Insurance renewals

- Holiday spending

- Birthdays

- Device repairs

- Home repairs

These expenses feel like emergencies when you do not prepare for them.

But many are not true emergencies. They are predictable expenses without a plan.

A sinking fund is money saved gradually for a future cost.

Example:

If you need $300 for school fees in three months, save $100 per month.

If you need $600 for annual insurance, save $50 per month.

If your phone usually needs repairs or replacement, set aside money slowly.

This protects your paycheck from being attacked by expenses you knew were coming.

A practical budget system must include sinking funds. Without them, you will keep being surprised by predictable costs.

Step 10: Handle Debt Without Letting It Control the Whole Budget

Debt is one of the biggest reasons people live paycheck to paycheck.

Debt payments reduce future income. This means your next paycheck arrives already weakened.

To take control, list all debts:

- Name of lender

- Balance

- Interest rate

- Minimum payment

- Due date

- Penalties

- Whether it is current or overdue

Then choose a repayment strategy.

Option 1: Debt Snowball

Pay the smallest debt first while making minimum payments on the others.

This gives quick wins and motivation.

Option 2: Debt Avalanche

Pay the highest-interest debt first while making minimum payments on the others.

This saves more money mathematically.

Which one is better?

If you need motivation, use the snowball method.

If you are disciplined and want to reduce interest faster, use the avalanche method.

But the most important rule is this:

Stop creating new debt while trying to repay old debt.

If you keep borrowing, repayment becomes a treadmill.

Also, do not use your entire emergency fund to pay debt unless you have a clear reason. You need some cash buffer, or the next emergency may push you back into borrowing.

Step 11: Build a Payday Routine

A payday routine is a repeated sequence you follow every time money arrives.

This is where the system becomes practical.

Use this order:

- Check total income received

- Move savings first

- Set aside bill money

- Set aside needs money

- Pay urgent bills

- Fund debt payments

- Divide flexible spending by week

- Update your budget tracker

- Check upcoming bills

- Leave only spendable money available

This routine should happen before celebration spending.

Do not go shopping first.

Do not order food first.

Do not send money randomly first.

Do not assume you have “extra” money first.

Payday is not the day to feel rich. Payday is the day to create order.

A good payday routine can change your entire financial life.

Step 12: Use Separate Accounts or Wallets

If all your money sits in one account, it becomes hard to know what is actually available.

You may look at your balance and think you have money, but some of that money is already meant for rent, bills, savings, or debt.

Separate accounts or wallets solve this.

You can create separate spaces for:

- Bills

- Food

- Transport

- Savings

- Emergency fund

- Flexible spending

This can be done with bank accounts, mobile wallets, cash envelopes, or budgeting apps.

The goal is not complexity. The goal is clarity.

When your flexible spending wallet is empty, you stop spending. You do not touch the bill money. You do not touch savings.

This system protects you from accidental overspending.

Step 13: Reduce Fixed Expenses Where Possible

Variable expenses matter, but fixed expenses can trap you.

Fixed expenses are repeated monthly costs that are hard to escape.

Examples:

- Rent

- Car payment

- Insurance

- Subscriptions

- Loan payments

- Phone plans

- Internet

- Memberships

If your fixed expenses are too high, your budget has very little room.

Look at your fixed expenses and ask:

- Can I negotiate this?

- Can I downgrade this?

- Can I cancel this?

- Can I share this cost?

- Can I switch providers?

- Can I delay this upgrade?

- Can I move to a cheaper option later?

Be careful: some fixed expenses cannot be changed quickly. Housing is one example. But even if you cannot change them this month, you can plan future changes.

If rent takes too much of your income, the long-term solution may involve moving, getting a roommate, increasing income, or renegotiating your living arrangement.

Do not ignore fixed expenses just because they are uncomfortable. They may be the reason your budget never works.

Step 14: Increase Income With a Specific Purpose

There is a limit to cutting expenses.

If your income is too low, you need an income plan.

But do not chase random money ideas without structure.

Choose one purpose:

“I need extra income to build a $500 buffer.”

or

“I need extra income to pay off my smallest debt.”

or

“I need extra income to cover transport without borrowing.”

This gives your extra work a clear mission.

Possible income options include:

- Weekend work

- Freelancing

- Tutoring

- Cleaning

- Delivery

- Selling food

- Reselling items

- Virtual assistance

- Social media services

- Writing

- Design

- Video editing

- Customer support

- Repair services

- Errands

Even an extra $25 per week creates $100 per month.

An extra $50 per week creates $200 per month.

An extra $100 per week creates $400 per month.

The mistake is earning extra money and spending it casually.

Every extra dollar must have a purpose.

Step 15: Review Your Money Every Week

A budget without review becomes outdated quickly.

Do a weekly money review.

Choose one day. Sunday works for many people, but any day is fine.

Ask:

- How much money do I have left?

- Which bills are due soon?

- Did I overspend in any category?

- Did I save what I planned?

- Did I use debt this week?

- What expense surprised me?

- What needs to change next week?

This review should take 15–30 minutes.

Do not turn it into a guilt session. The goal is correction.

If you overspent, identify why. If the budget was unrealistic, adjust it. If you forgot a bill, add it to the calendar. If food costs were too high, plan meals better next week.

The people who escape paycheck-to-paycheck living are not perfect. They review, adjust, and repeat.

A Practical 30-Day Plan to Stop Living Paycheck to Paycheck

Here is a simple first-month plan.

Week 1: Get Clear

Actions:

- List all income

- List all bills

- List all debts

- Track all spending

- Create a bill calendar

- Choose a first savings target

Goal:

Know your real financial position.

Do not try to fix everything yet. Just get honest.

Week 2: Build the System

Actions:

- Create the four-bucket budget

- Separate bill money from spending money

- Start saving a small amount first

- Set weekly spending limits

- Cancel or reduce three cash leaks

Goal:

Stop money from disappearing without a plan.

Week 3: Create Breathing Room

Actions:

- Start a small buffer

- Sell unused items

- Try a no-spend weekend

- Reduce food or transport waste

- Make minimum debt payments on time

Goal:

Create the first gap between you and zero.

Week 4: Strengthen the Routine

Actions:

- Review the budget

- Adjust unrealistic categories

- Create sinking funds for predictable expenses

- Choose one income improvement action

- Plan next month before it starts

Goal:

Move from reaction to control.

This 30-day plan will not make you rich. But it can stop the bleeding. That is the first win.

A Sample Budget for Someone Living Paycheck to Paycheck

Let’s say monthly income is $1,500.

Example budget:

- Rent: $500

- Utilities: $120

- Food: $300

- Transport: $150

- Phone/internet: $60

- Debt minimums: $150

- Emergency fund: $50

- Sinking funds: $50

- Flexible spending: $120

Total: $1,500

At first, saving $50 may not seem impressive. But if this person previously saved nothing, that is progress.

The next goal is to reduce leaks or increase income so savings can grow from $50 to $100, then $150.

Financial progress often begins slowly. That does not make it useless.

What If Your Expenses Are Higher Than Your Income?

This is serious.

If your expenses are higher than your income, budgeting alone cannot solve the full problem. A budget will reveal the truth, but you still need action.

You have four options:

- Reduce expenses

- Increase income

- Restructure debt

- Get temporary support while rebuilding

Start by identifying the gap.

Example:

Income: $1,500

Expenses: $1,750

Gap: $250

Now the question becomes:

How do you close the $250 gap?

Possible actions:

- Cut $75 from food waste and subscriptions

- Reduce transport by $40

- Negotiate or restructure one bill

- Earn $150 extra per month

- Pause non-essential spending

You need a gap-closing plan.

Ignoring the gap creates debt.

Common Mistakes That Keep People Paycheck to Paycheck

Mistake 1: Budgeting After Spending

By then, the damage is done. Budget before spending.

Mistake 2: Saving Only When There Is Extra

There is rarely extra. Save first.

Mistake 3: Treating Credit Like Income

Credit is not income. It is future pressure.

Mistake 4: Ignoring Small Expenses

Small repeated expenses are often the leak.

Mistake 5: Having No Bill Calendar

Bills should not surprise you every month.

Mistake 6: Not Building a Buffer

Without a buffer, every problem becomes an emergency.

Mistake 7: Copying Someone Else’s Budget

Your budget must fit your income, expenses, and responsibilities.

Mistake 8: Giving Up After One Bad Week

Adjust the system. Do not abandon it.

Signs You Are Breaking the Cycle

You will know the system is working when:

- You know where your money goes

- You are not surprised by bills

- You save something every payday

- You borrow less often

- You have a small emergency buffer

- You spend less impulsively

- You review money weekly

- Your paycheck lasts longer

- You feel less panic before payday

The biggest sign is this:

You stop feeling like money controls you.

Even if progress is slow, control changes everything.

Conclusion: You Need a System, Not Just More Willpower

If you want to learn how to stop living paycheck to paycheck, the answer is not simply “spend less.”

That advice is too shallow.

You need a system that tells your paycheck what to do before life, pressure, bills, emotions, and impulse spending take over.

Start by facing your real numbers. Map your paycheck. Use the four-bucket budget. Save first, even if it is small. Build a buffer. Control weekly spending. Create a bill calendar. Cut cash leaks. Prepare for irregular expenses. Handle debt carefully. Review your money every week.

This will not fix everything overnight. But it will change the direction.

The first goal is not wealth. The first goal is breathing room.

Then stability.

Then control.

Then growth.

Living paycheck to paycheck can feel permanent when you are inside the cycle. But it is not permanent if you build a better system and repeat it long enough.

Your paycheck should not disappear without a plan.

Give every dollar a job, protect your future before spending begins, and build the first gap between you and financial panic. That gap is where your financial life starts to change.

Frequently Asked Questions

Why do I keep living paycheck to paycheck even with a decent income?

Living paycheck to paycheck is usually caused by lifestyle inflation, no budget, untracked spending, and the absence of automated savings. When spending rises with income and nothing is saved first, there is nothing left at the end of the month regardless of how much you earn.

What is the first step to stop living paycheck to paycheck?

The first step is to track every dollar you spend for 30 days without changing anything. You cannot fix what you cannot see. Once you know exactly where your money is going you can identify the leaks and build a realistic budget around your actual spending patterns.

How much should I save before I stop feeling broke?

Start with a $1,000 emergency fund. This single step breaks the paycheck to paycheck cycle for most people because it gives you a buffer when unexpected expenses happen. Without it every surprise expense sends you back to zero or into debt.

What is the best budget system to stop living paycheck to paycheck?

The best budget systems for breaking the paycheck to paycheck cycle are zero based budgeting and the 50/30/20 rule. Zero based budgeting gives every dollar a job so nothing is wasted. The 50/30/20 rule is simpler and works well for beginners who need a starting framework.

How do I stop living paycheck to paycheck on a low income?

On a low income focus on three things — reduce your biggest expenses, eliminate cash leaks like subscriptions and food delivery, and save a small fixed amount every payday before spending anything else. Even saving $25 per week builds momentum and breaks the cycle over time.

Should I use cash or a card to stop overspending?

Cash envelopes work better for people who overspend with cards. When you physically hand over cash you feel the cost more than swiping a card. Use cash for your highest problem spending categories like groceries, dining, and entertainment until you build better spending habits.

How long does it take to stop living paycheck to paycheck?

Most people see meaningful improvement within 60 to 90 days of following a consistent budget. Building a full emergency fund and feeling financially stable typically takes 6 to 12 months. The key is consistency — small improvements every month add up faster than most people expect.

John F. Miller is a personal finance writer and the founder of MyCash Advice. He covers savings accounts, credit cards, budgeting strategies, and debt payoff methods. His mission is to make practical money advice accessible to everyone regardless of income level.