Why You’re Still Broke: 12 Money Habits Keeping You Stuck

Introduction: Being Broke Is Not Always About Laziness

If you are still broke, the easiest explanation is usually the most insulting one: “You are just bad with money.”

That explanation is too simple.

Yes, personal choices matter. Spending habits matter. Discipline matters. But being broke is often the result of several problems working together: low income, poor budgeting, debt, lifestyle pressure, lack of savings, weak financial education, and emotional spending.

The hard truth is this:

Many people are not broke because of one big mistake. They are broke because of repeated small decisions, weak systems, and financial pressure that never gives them room to recover.

That does not mean you are powerless. It means you need to stop looking for one magic fix.

If you want to understand why you’re still broke, you need to examine the full pattern: how money comes in, how money leaves, what habits control your spending, and what systems you have failed to build.

This article breaks down the most common reasons people stay broke and what to do instead.

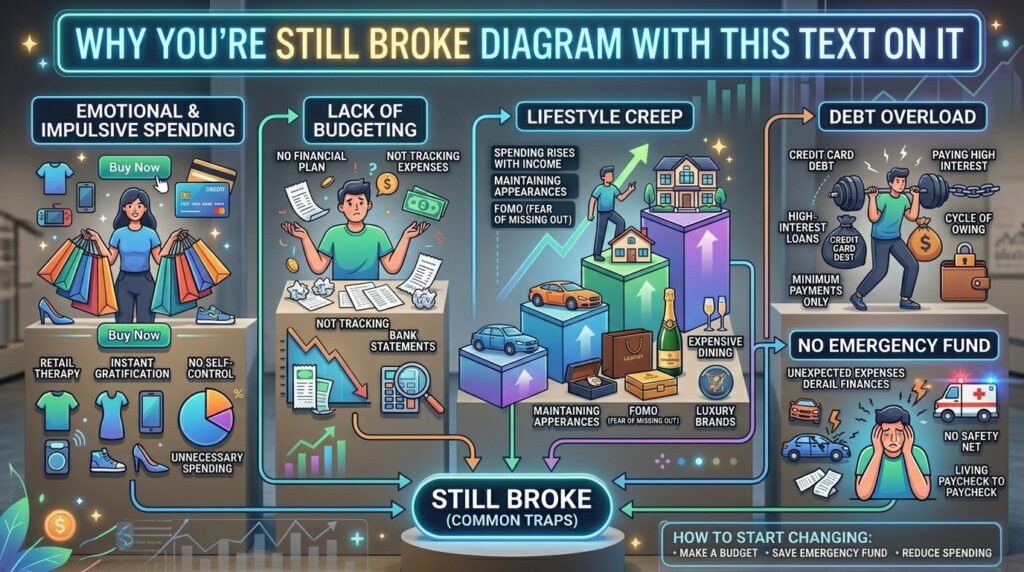

1. You Don’t Know Where Your Money Goes

This is one of the biggest reasons people stay broke.

They earn money. They spend money. Then they wonder where it went.

If you do not track your money, your financial life becomes guesswork. You may think rent is the main problem. You may think food is the main problem. You may blame bills, transport, family support, or low income.

Some of those may be real issues. But without tracking, you do not know the exact damage.

Money often disappears through small spending:

- Snacks

- Takeout

- Delivery fees

- Random online purchases

- Subscriptions

- Transport upgrades

- Data bundles

- Impulse shopping

- Unplanned social spending

Each expense may look small alone. The problem is repetition.

A $5 expense is not just $5 if it happens 20 times a month. That becomes $100. A $10 impulse purchase repeated weekly becomes $40 a month. Small leaks become large losses.

If you want to stop being broke, start by tracking your spending for 30 days. Do not judge yourself during the first week. Just observe.

Write down:

- What you bought

- How much it cost

- Why you bought it

- Whether it was planned or emotional

The goal is not shame. The goal is clarity.

You cannot fix invisible spending.

2. You Save Whatever Is Left Over

This is a broken saving strategy.

Most people spend first and hope to save later. But by the time later comes, the money is gone.

This is one of the clearest answers to why you’re still broke: you treat saving as optional.

Saving cannot be the leftover category. It must be a planned category.

If you wait until the end of the month to save, you are depending on luck. Bills, food, transport, family needs, emergencies, and impulse spending will usually win.

The better method is simple:

Save first, then spend what remains.

This does not mean saving a huge amount immediately. If your income is tight, start small.

You can save:

- 1% of every payment

- 5% of every paycheck

- $5 per week

- $20 per month

- Any fixed amount that builds the habit

The habit matters because it changes the order of your financial life.

Saving first tells your brain: “This money is protected.”

If you are currently broke, your first goal is not to become rich. Your first goal is to stop starting from zero every month.

If you need a practical saving system, read how to save money fast on a low income.

3. Your Budget Is Either Missing or Unrealistic

A budget is not a punishment. It is a plan.

But many people either have no budget or build one that has no connection to real life.

A weak budget says:

- “I will stop eating out completely.”

- “I will spend almost nothing on fun.”

- “I will save half my income.”

- “I will never make impulse purchases again.”

That may look good on paper, but it usually collapses.

A good budget must be realistic enough to survive your actual life.

If your budget does not include transport, food variation, small emergencies, family obligations, personal spending, and occasional mistakes, it will fail.

The point of budgeting is not to create a fantasy version of yourself. It is to manage the version of yourself that currently exists while slowly improving your behavior.

A simple beginner budget should include:

- Housing

- Food

- Transport

- Utilities

- Debt payments

- Savings

- Emergency fund

- Personal spending

- Miscellaneous

The “miscellaneous” category matters because life is not perfectly predictable. If you do not plan for irregular spending, your budget will break every time something unexpected happens.

If you need help creating a simple system, read budgeting for beginners.

4. You Confuse Income With Financial Progress

Earning more money helps, but income alone does not fix bad money behavior.

Many people earn more and still remain broke because their spending rises with their income. This is called lifestyle inflation.

The pattern is simple:

- You earn more

- You upgrade your lifestyle

- Your expenses increase

- You still save nothing

- You feel broke again

More income only helps if you use it to create financial distance between what you earn and what you spend.

If every increase in income becomes a new phone, better clothes, more eating out, expensive subscriptions, upgraded housing, or unnecessary shopping, you will stay financially stuck.

This is why some people with modest incomes save money while others with higher incomes are constantly broke.

The difference is not always income. Sometimes it is financial structure.

When your income increases, decide in advance where the extra money will go.

A strong rule is:

- Save part of the increase

- Use part to pay debt

- Keep part for lifestyle improvement

This lets you enjoy progress without destroying your future.

If you spend every raise before it stabilizes you, you are not growing. You are just expanding your bills.

5. You Use Debt to Maintain a Lifestyle You Cannot Afford

Debt is one of the fastest ways to stay broke.

Some debt may be strategic, such as a reasonable mortgage, business loan, or education loan. But consumer debt used for lifestyle spending is dangerous.

This includes debt used for:

- Clothes

- Eating out

- Vacations

- Gadgets

- Parties

- Non-essential upgrades

- Impulse purchases

- Keeping up appearances

The problem is not only the amount borrowed. The problem is that debt pulls money from your future income.

Before your next paycheck arrives, part of it already belongs to someone else.

That creates a cycle:

- You borrow because money is tight

- Repayments reduce your next income

- Your next income becomes too small

- You borrow again

- The cycle continues

If you are asking why you’re still broke, look closely at your debt. Debt may be quietly eating your future before you even reach it.

Start by listing:

- Every debt

- Total balance

- Interest rate

- Minimum payment

- Due date

- Penalties

Then prioritize high-interest debt first. Expensive debt is financial quicksand. The longer it sits, the harder it becomes to escape.

If your paycheck disappears before the month ends, read how to stop living paycheck to paycheck.

6. You Spend to Feel Better

Emotional spending is real.

People spend when they are stressed, bored, lonely, tired, embarrassed, excited, or trying to feel in control.

The purchase gives a temporary emotional reward. But when the feeling fades, the financial problem remains.

Common emotional spending patterns include:

- Buying clothes to feel confident

- Ordering food because the day was stressful

- Shopping online when bored

- Spending on friends to avoid feeling left out

- Buying gadgets to feel successful

- Paying for entertainment to escape pressure

This does not mean every enjoyable purchase is bad. Money should support life, not just bills.

The problem is when spending becomes emotional medicine.

If you repeatedly spend to manage feelings, your budget will never hold.

Before buying something non-essential, pause and ask:

- Am I buying this because I need it?

- Am I buying this because I feel bad?

- Will I still value this tomorrow?

- Is there a cheaper way to meet the same emotional need?

Sometimes the solution is not another purchase. Sometimes it is rest, conversation, planning, exercise, prayer, journaling, or simply waiting 24 hours.

A practical rule:

Delay all non-essential purchases by 24 hours.

If you still want it tomorrow and it fits the budget, consider it. If not, you just saved money.

7. You Keep Financially Comparing Yourself to Others

Comparison is expensive.

Many people are broke because they are trying to look financially better than they are.

They buy things to signal success:

- Better clothes

- Better phone

- Better car

- Better apartment

- Better restaurants

- Better lifestyle photos

- Better vacations

But looking stable and being stable are not the same thing.

Social media makes this worse because you are constantly exposed to other people’s highlights. You see the purchase, not the debt. You see the vacation, not the credit card balance. You see the car, not the monthly payment.

If your spending is driven by comparison, you will always need more.

Someone will always have more expensive clothes. Someone will always travel more. Someone will always live somewhere nicer. Someone will always seem ahead.

The way out is to define your own financial priorities.

Ask:

- What do I actually want my money to do for me?

- Do I want peace or applause?

- Do I want savings or appearances?

- Do I want freedom or approval?

Being broke often continues when public image matters more than private stability.

Choose stability.

8. You Have No Emergency Fund

Without an emergency fund, every problem becomes a crisis.

A phone repair becomes debt. A medical bill becomes panic. A missed workday becomes financial damage. A family emergency wipes out your budget.

This is another major reason why you’re still broke: you have no buffer between life and your money.

An emergency fund protects you from being pushed backward by every surprise.

Start small.

Your first emergency fund goal does not need to be three to six months of expenses. That advice may be too big for someone starting from zero.

Start with:

- $100

- Then $250

- Then $500

- Then $1,000

The first $100 matters because it stops you from being completely exposed.

Keep emergency money separate from daily spending money. If it sits in the same account, you will probably use it.

For a full savings plan, read the emergency fund guide.

9. You Do Not Increase Your Earning Power

Cutting expenses matters. But there is a limit to how much you can cut.

If your income is too low, budgeting alone will not fix everything. At some point, you need to increase earning power.

This does not mean chasing random side hustles every week. That becomes chaotic.

It means deliberately improving your ability to earn.

Ways to increase earning power include:

- Learning a marketable skill

- Improving communication

- Building digital skills

- Taking certifications

- Freelancing

- Starting a small service business

- Negotiating pay

- Applying for better roles

- Selling useful products

- Building a portfolio

- Becoming more valuable in your field

Many people stay broke because they only focus on survival. They never build the skills or systems that can increase income.

That is understandable, but dangerous.

If you spend all your energy only managing shortage, you may never create growth.

Pick one skill that can improve your income over the next 6–12 months. Focus on it seriously.

Examples:

- Writing

- Sales

- Design

- Video editing

- Coding

- Bookkeeping

- Social media management

- Digital marketing

- Data analysis

- Customer service

- Virtual assistance

Income growth should not be random. It should be intentional.

10. You Invest Before You Are Ready

Investing is important, but investing too early or recklessly can make your situation worse.

Some people are still broke because they jump into investments without financial stability.

They invest while:

- They have no emergency fund

- They have high-interest debt

- They do not understand the investment

- They are chasing hype

- They are using borrowed money

- They need the money soon

That is not investing. That is gambling under pressure.

Before investing, you need:

- Basic emergency savings

- Clear goals

- Stable cash flow

- Understanding of risk

- No dependence on invested money for urgent bills

Investing should help you build wealth over time. It should not be a desperate attempt to escape being broke quickly.

If you are new to investing, read how to start investing with no experience.

11. You Have No Financial System

A financial system is a repeatable way of handling money.

Without a system, every paycheck becomes a fresh battle.

A basic financial system includes:

- Payday routine

- Budget categories

- Automatic savings

- Bill schedule

- Debt repayment plan

- Emergency fund

- Weekly money review

- Spending limits

- Long-term goals

If you do not have a system, you depend on memory, mood, and discipline. That is unreliable.

A simple payday system might look like this:

- Income arrives

- Savings transferred first

- Bills paid or set aside

- Debt payment allocated

- Food and transport budget assigned

- Flexible spending separated

- Weekly review scheduled

This system does not need to be fancy. It needs to be repeatable.

The people who improve financially are not always the smartest. They are often the ones with the clearest systems.

12. You Keep Restarting Instead of Adjusting

One bad week does not mean your plan failed.

Many people create a budget, overspend once, feel guilty, and quit. Then they restart weeks later. This cycle repeats for years.

That is how people stay broke.

Financial progress does not require perfect execution. It requires correction.

If you overspend, do not abandon the budget. Ask:

- What caused the overspending?

- Was the budget unrealistic?

- Did I forget an expense?

- Was the purchase emotional?

- Do I need a better category?

- What adjustment prevents this next time?

A budget is a working document. It should evolve.

The goal is not to never make mistakes. The goal is to stop making the same mistake without learning from it.

You do not need a perfect month. You need a better system.

How to Stop Being Broke: A Simple Recovery Plan

Now that the causes are clear, here is a practical plan.

Step 1: Track Every Expense for 30 Days

Do not skip this. Guessing is not enough.

Track all money leaving your hands.

Step 2: Build a Basic Budget

Use simple categories:

- Needs

- Savings

- Debt

- Flexible spending

- Emergency fund

Step 3: Save First

Move money into savings immediately when income arrives.

Step 4: Cut 3 Money Leaks

Choose three recurring expenses to reduce this month.

Step 5: Build a $100 Emergency Fund

Start small. Build the habit.

Step 6: Stop New Bad Debt

Do not borrow for lifestyle expenses.

Step 7: Increase Income Intentionally

Pick one skill, service, or opportunity to grow income over time.

Step 8: Review Weekly

Every week, check your money and adjust.

This plan is not complicated. But it works only if you execute consistently.

Frequently Asked Questions

Why do I have no money even though I work hard?

The most common reasons are lifestyle inflation, no budget, impulse spending, and not tracking expenses. Earning more money does not solve the problem if your spending habits stay the same.

What are the worst money habits?

The worst money habits include living paycheck to paycheck, not saving, carrying credit card debt, buying things on impulse, and not having an emergency fund.

How do I stop being broke?

Start by tracking every dollar you spend for 30 days. Then create a simple budget, cut unnecessary expenses, build a $1,000 emergency fund, and automate your savings.

How long does it take to improve your finances?

You can see meaningful improvement in 90 days with consistent effort. Building a solid financial foundation typically takes 6 to 12 months of disciplined budgeting and saving.

John F. Miller is a personal finance writer and the founder of MyCash Advice. He covers savings accounts, credit cards, budgeting strategies, and debt payoff methods. His mission is to make practical money advice accessible to everyone regardless of income level.